As the industry approaches this absolute production cost-floor, the battle between the two primary growing technologies—Chemical Vapor Deposition (CVD) and High-Pressure High-Temperature (HPHT)—has shifted from a race for pure carat volume to an aggressive war over utility-margin optimization.

The multi-year price collapse in lab-grown diamonds (LGD) is entering a new, structural phase. According to recent data, polished wholesale prices have stabilized near a cost-floor, dropping only about 2.6% year-over-year compared to the double-digit crashes of 2022–2024. As the industry approaches this absolute production cost-floor, the battle between the two primary growing technologies—Chemical Vapor Deposition (CVD) and High-Pressure High-Temperature (HPHT)—has shifted from a race for pure carat volume to an aggressive war over utility-margin optimization.

Tech Breakdown: The Margin War Behind the Tech

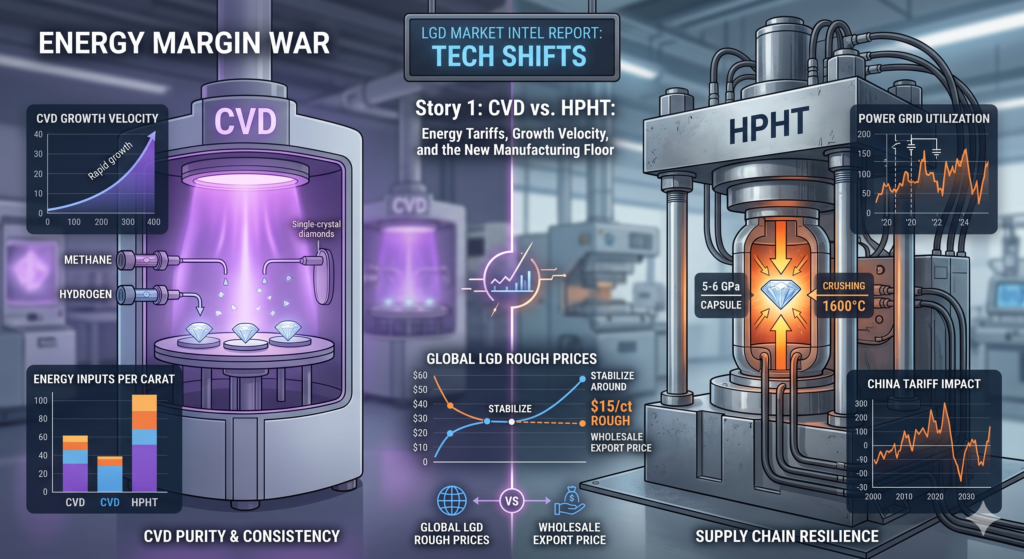

While HPHT still commands roughly 54% of the manufacturing market share (primarily due to its historic dominance in volume output and smaller, melee-sized stones), CVD is expanding at the fastest compound annual growth rate. The reason is simple: energy inputs.

1. The Energy Tariff Crunch (India vs. China)

The geographical divide in LGD production is highly tech-dependent:

China remains the powerhouse for HPHT production, repurposing massive industrial diamond presses (originally used for abrasive tools) in regions like Henan.

India has heavily invested in CVD reactor farms, notably backed by government initiatives like the India Centre for Lab-Grown Diamonds (InCent-LGD).

The B2B Data Pivot: HPHT requires massive, continuous electrical loads to maintain pressures of 5–6 GPa and temperatures up to 1600°C. In contrast, modern CVD plasma reactors operate at lower pressures, resulting in lower energy costs per carat. As global energy tariffs fluctuate, Indian CVD producers are proving more resilient to power grid price spikes than China’s heavy-iron HPHT grid dependencies.

2. Growth Velocity & Inventory Turnaround

Time is money when wholesale prices are tight.

Modern CVD processes can grow high-purity, jewelry-grade Type IIa diamond crystals within a matter of weeks.

Because CVD allows for precise chemical tuning via methane gas injection, manufacturers can scale production up or down much faster than an HPHT facility can fire up or cool down massive hydraulic cube presses.

Market Intel: The “$15 Rough” Reality

To understand why production tech efficiency matters so much to B2B buyers right now, look at the raw import data. In mid-2026, the average import value of rough LGD entering major cutting centers like Surat, India, sits at a staggering $15 per carat.

| Metric | Mined Equivalent | Lab Wholesale (Polished) | Lab Rough (Input Cost) |

| Avg. Cost Per Carat | ~$2,000 – $5,000+ | ~$74 – $100 | ~$15 |

With only a roughly $60–$80 spread between rough input costs and polished wholesale export prices, there is zero room for operational inefficiency. If a manufacturer’s energy bill spikes by even 10%, their entire margin on that batch is wiped out.

💡 Why This Matters to B2B Buyers & Wholesalers

Predicting the Price Floor: If buyers know that $15/ct rough is the baseline for China/India production, they can safely assume polished wholesale prices (currently around $564 for a 1-carat stone on retail-ready indices) are stabilizing. The risk of sudden inventory devaluation is lower than it was two years ago.

CVD Purity is a Selling Point: Because CVD allows for exact gas control, it is yielding highly predictable, high-clarity colorless stones without the metallic flux inclusions sometimes found in cheaper HPHT runs. Wholesalers should use this tech shift to pitch “purity consistency” to retail jewelers.

The Supply Chain Pivot: India’s loose LGD export volumes have officially crossed a historic threshold, surpassing natural diamond export volumes. Buyers looking for stable supply lines are increasingly shifting contracts toward Indian CVD tech clusters to insulate themselves from Chinese industrial grid policies.